“Data is the new oil…”

“Lithium is the new oil…”

“Processing power is the new oil…”

As we near the mid point of 2026, the ‘new oil’ analogy feels like a relic of a simpler time. Geopolitical headaches aside, oil is a relatively simple commodity to extract, refine, and ship.

But the minerals currently dictating the fate of the U.S. economy (minerals like antimony, gallium, neodymium, and high purity copper), are a different beast entirely.

From the data centers powering our generative AI to the munitions defending our borders, today’s “new oil” is a complex list of elements that U.S. procurement professionals across multiple sectors are currently scrambling to secure.

What Makes a Mineral "Critical?"

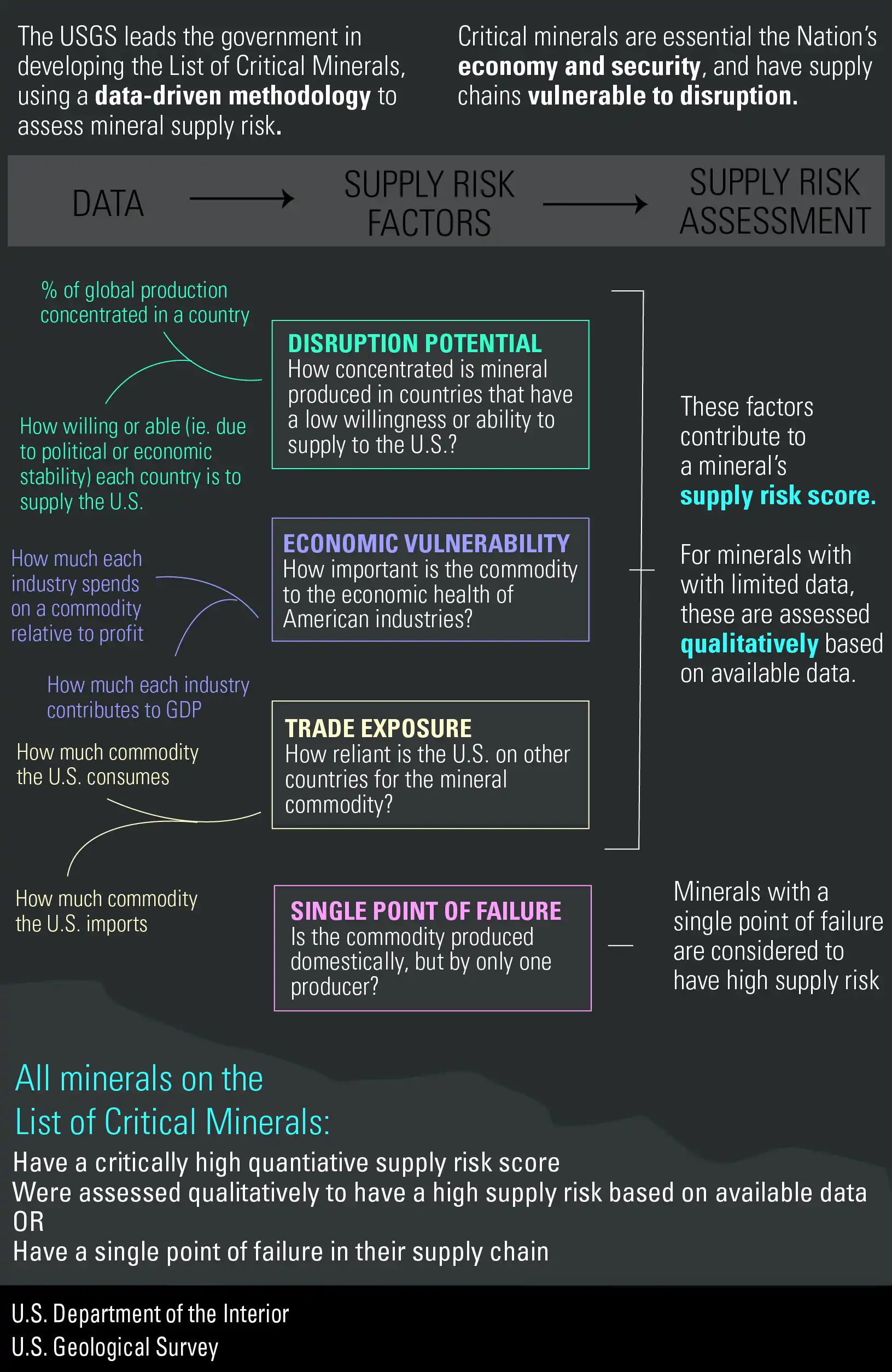

Before we dive into the specific crunches, it’s important to understand the criteria for the list. According to the U.S. Geological Survey, a mineral is not labeled critical simply because it is rare. It earns that title through a data driven assessment of supply risk.

The government evaluates four factors to determine criticality:

- Disruption Potential: This measures how much of a mineral is produced in countries that may be unwilling or unable to supply the U.S. due to political or economic instability.

- Economic Vulnerability: This looks at how essential a commodity is to the economic health of American industries and its overall contribution to the GDP.

- Trade Exposure: This tracks how reliant the U.S. is on foreign nations for a specific mineral versus what we can produce at home.

- A mineral might also be deemed critical if it has a single point of failure, meaning it is produced domestically but only by one single producer. If any of these scores are high, the mineral becomes a matter of national security.

The Critical Minerals in Question

Here is where the pressure points are at their sharpest.

1. Antimony

If you have not been tracking antimony, your risk management team likely has. Essential for everything from armor-piercing ammunition to flame retardants and night-vision goggles, antimony is the definition of a point-of-failure mineral.

The U.S. remains dangerously dependent on China, Tajikistan, and Russia for the lion’s share of its sourcing. With global tensions remaining high, the U.S. Department of Energy has pivoted toward domestic antimony recovery. The focus is now on who has the chemical processing capacity to turn those rocks into military-grade alloys.

2. Gallium

Your AI strategy is only as fast as your gallium supply. This niche metal is the backbone of high-performance semiconductors and 5G and 6G infrastructure. Right now, China controls roughly 98 percent of global gallium refining.

American businesses have learned that near-shoring the mine offers little help if the refining stays overseas. The U.S. is currently pouring billions into closed loop processing facilities to bypass the 2025 export restrictions that nearly crippled the domestic laser and sensor industry.

3. High-Purity Copper

We used to think of copper as a base metal. The explosion of AI data centers has turned copper into a high stakes luxury.

An AI data center requires significantly more copper for power distribution than a traditional one. Coupled with the massive electrification of the U.S. grid, we are facing a structural shortfall that recycling alone cannot fix. Declining ore grades in traditional mines mean we are working harder for less.

Procurement teams are now looking at long-term price floors to incentivize new, technologically complex domestic projects that were previously too expensive to greenlight.

4. Neodymium and Praseodymium

You can’t build a high-efficiency EV motor without permanent magnets, and you can’t build those magnets without these two elements.

While the U.S. has ramped up mining at sites like Mountain Pass, the downstream magnet-making expertise is still catching up. The focus has shifted toward separating these elements from the sludge. The 2026 trend is all about solvent extraction technology to meet environmental standards and cost competitiveness.

5. Lithium and Graphite

The lithium boom of the early 2020s has matured into a more nuanced market. While prices have stabilized compared to the 2022 spikes, the supply chain remains brittle.

Synthetic graphite is essential for battery anodes and is energy intensive to produce. As U.S. electricity prices rise due to AI demand, the cost of making graphite domestically is hitting a wall.

Your Critical Mineral Strategy for 2026

Here’s the full list of critical minerals from the USGS (updated November 2025). If having access to one or more of these minerals has the potential to make or break your organization, consider the following three key shifts in strategy:

- Look Deep into the Sub Tiers: You buy the minerals inside your parts. Mapping your Tier 3 and Tier 4 suppliers is a survival tactic.

- Invest in Processing: The real white space for innovation is in the refining and processing facilities.

- Collaborative Sourcing: No single company can move the needle on a global mineral crunch. We are seeing a return to ecosystem procurement where industry players and governments work together to guarantee demand through offtake agreements.

Let Una take care of your indirect spend

While the global mineral crunch puts pressure on your direct materials, joining a GPO like Una can help you master your indirect spend, from IT infrastructure to industrial supplies, to ensure your operation stays lean and focused on the big picture.

Contact us to learn more.